Acme Insurance

Executive Summary

By focusing on its strengths, its present client base, and new value priced products in the next year, Acme Insurance plans to increase gross sales by 10% and profit by 15%.

Our Keys to Success and critical factors for the next year are, in order of importance:

- Identify “Target Markets.”

- Institute our Property inspection program.

- Begin our “Insurance Partners” program.

- Develop a profitable property program.

- Provide small businesses with an affordable basic business package.

Acme Insurance Incorporated has been profitable, but recently we have had declining market share and this must be addressed. Therefore our goals are:

- To re-establish Acme Insurance Inc. as the market leader in quality and value-priced insurance products in Smalltown District.

- Establish good working relationships with our present insurance markets by meeting with their decision makers and plotting a mutual plan for success. Get commitments for support and products that we can market in our trading area starting April 1st of Year 1.

- Investigate new markets that meet our marketing criteria by a) committing to small rural brokerage; b) providing products suitable to our economic and social climate; and c) plans for the upload and download of insurance policies.

- Provide sales incentives to staff to meet sales goals of 10%.

- Complete inspection of all Pilot homeowners within one month before renewal date.

- Formulate plans to acquire another brokerage

Acme Insurance Inc. is dedicated to providing insurance products that provide quality protection with value pricing. We wish to establish a successful partnership with our clients, our staff members, and our insurance companies, that respect the interests and goals of each party.

Success will be measured by our clients choosing us because of their belief in our ability to meet or exceed their expectations of price, service, and expertise.

In order to implement our strategic goals, we will focus on developing the following tools.

- Knowledgeable, friendly staff that can empathize with our consumers needs and circumstances, especially in handling a loss.

- Policies that meet or exceed the expectations of our clients, and that are affordable, available, and understandable.

- Policies and endorsements delivered on time with minimal errors.

- A commitment to an annual insurance review for all of our clients. A phone call is more than any direct mass marketer offers. We believe personal contact and service is the cornerstone of our success.

Acme Insurance primarily markets and services Personal Lines Insurance. Its customers are mostly rural, lower income families or long time resident senior citizens who demand value priced insurance premiums in keeping with their lower and fixed incomes.

We also provide insurance to small business, mostly family-run seasonal operations primarily focused on the tourist trade.

Acme Insurance is a privately incorporated company in the Smalltown district and is licensed to transact both Life and General Insurance. The shares are held equally by John Smith and Peter Smith.

Our Insurance and Real Estate brokerage operates from two central locations. Our modern attractive office in Smalltown, at 178 Small Street, is located in a small plaza which is owned by the principals of our brokerage. It comprises 2,000 square feet.

In Nexttown, we operate from an 800 square foot, one-story brick veneer building overlooking Lake Small, which again is owned by the principals of our firm. The office is strategically located across from the Post Office.

We have stressed to our insureds the importance of good communication between the broker and client to insure proper coverage is in place. We have noticed as our clients become better informed about insurance that there has been a tremendous increase in clients wishing in-depth discussions about their policy coverage and how they can get the most value for their insurance dollar.

Our company’s strength lies in the quality and depth of our products and staff. Our offices, unlike our competition, are open six days a week. Because of our larger staff, we are able to service our clients even when a client’s broker is busy or out of the office on inspections.

Our staff has specialists in commercial insurance that can properly service and underwrite local business. We also have some quality commercial markets unavailable to our competition.

Our Real Estate division, which is a separate company, helps with market value and replacement cost analysis when required.

The past few years have seen tremendous upheaval in the insurance industry. The number of players has decreased in both the broker and company communities. The recession has curtailed insureds from properly maintaining their homes and automobiles, and insurance fraud has become a major issue for the entire insurance industry.

Brokers are concerned that in spite of commission reductions, quotas, contract cancellations, and refusal to write new auto business by some markets, they now may find themselves in competition with some of the traditional broker distribution companies that are setting up direct marketing facilities and branches. The banks now have announced they will open stand alone insurance offices to retail insurance.

In spite of the above, we believe that the independent broker will survive. We are more automated than most service industries. We are close to the customer, regardless of some insurance companies’ attempts to sever the traditional broker-client relationship. Our clients, in most cases, still do not care or know which company we place them with. They trust our judgement in selecting the proper coverage and company to place them in.

Upload/download capabilities are in many brokers offices, including our own. This will cut costs, improve efficiency and accuracy, and help us meet the competition from banks and direct writers. Companies that truly value and trust the broker distribution system will align themselves with professional brokers and grant more underwriting authority similar to Lloyds.

Among the substitutes that are our main competition we have Local independent brokers, Agents (such as Co-operators), Mass Markets, Mass merchandise programs heavily advertised over the radio such as “Gray Power”, and Group Plans.

We have depended in the past on a small advertisement in our local newspaper, listings in the Yellow Pages, and word of mouth. However with the changes in the market today, we must begin to investigate alternate ways to put our name in front of the public. We have set out several criteria for our marketing campaign that include”

- All advertising has to emphasize our differentiation point rather than price.

- We must sell the company, not the product. In spite of some companies’ efforts to minimize the importance of the broker, our clients still identify with the broker, not the insurance company.

- We must improve and increase our contacts with our clients.

- Make contacts and support senior citizen groups and cottage associations.

Based on these changes in our goals, outlook, and company culture, we anticipate that we will be able to increase revenues substantially by year 3 of the plan and increase net profit handsomely. The company does not anticipate any cash flow problems.

1.1 Mission

Acme Insurance Inc. is dedicated to providing insurance products that provide quality protection with value pricing. We wish to establish a successful partnership with our clients, our staff members, and our insurance companies, that respect the interests and goals of each party.

Success will be measured by our clients choosing us because of their belief in our ability to meet or exceed their expectations of price, service, and expertise.

1.2 Objectives

- To re-establish Acme Insurance Inc. as the market leader in quality and value-priced insurance products in Smalltown District.

- Establish good working relationships with our present insurance markets by meeting with their decision makers and plotting a mutual plan for success. Get commitments for support and products that we can market in our trading area starting April 1st of Year 1.

- Investigating new markets that meet our marketing criteria by a) committing to small rural brokerage; b) providing products suitable to our economic and social climate; and c) plans for the upload and download of insurance policies.

- Provide sales incentives to staff to meet sales goals of 10%.

- Complete inspection of all Pilot homeowners within one month before renewal date.

- Formulate plans to acquire another brokerage.

1.3 Keys to Success

We believe the keys to success in a small town insurance business are:

- Knowledgeable, friendly staff that can empathize with our consumers needs and circumstances, especially in handling a loss.

- Policies that meet or exceed the expectations of our clients, and that are affordable, available, and understandable.

- Policies and endorsements delivered on time with minimal errors.

- A commitment to an annual insurance review for all of our clients. A phone call is more than any direct mass marketer offers. We believe personal contact and service is the cornerstone of our success.

Company Summary

Acme Insurance primarily markets and services Personal Lines Insurance. Its customers are mostly rural, lower income families or long time resident senior citizens who demand value priced insurance premiums in keeping with their lower and fixed incomes.

We also provide insurance to small business, mostly family-run seasonal operations primarily focused on the tourist trade.

2.1 Company Ownership

Acme Insurance is a privately incorporated company in the Smalltown district and is licensed to transact both Life and General Insurance. The shares are held equally by John Smith and Peter Smith.

2.2 Company History

Acme Insurance was founded as a sole proprietorship in 1938 and was owned and operated by the founder Stan Smith. He originally ran the operation from his home, but moved to the business section of Smalltown when he outgrew his home based operation.

In 1972, the company constructed a new office building in the main business section and over the course of the last 15 years has purchased four other brokerages, one of which led to the establishment of our branch office in Nexttown.

In 1988, a new company was formed “Acme Insurance Inc.” which bought the insurance business from “Acme Insurance Limited.” All shares in the new company are owned by John S. Smith and Peter Smith.

Today, the fourth generation of Smiths, Stephen and Jason Smith, are working in the firm. We are also gratified to report that our founder, Stan Smith, is still in our office every day, and although still licensed, he is only active in a “goodwill ambassador” capacity.

| Past Performance | |||

| 1993 | 1994 | 1995 | |

| Sales | $644,023 | $660,593 | $622,309 |

| Gross Margin | $144,174 | $115,204 | $120,525 |

| Gross Margin % | 22.39% | 17.44% | 19.37% |

| Operating Expenses | $597,440 | $604,559 | $560,266 |

| Collection Period (days) | 0 | 0 | 0 |

| Balance Sheet | |||

| 1993 | 1994 | 1995 | |

| Current Assets | |||

| Cash | $0 | $0 | $402,640 |

| Accounts Receivable | $0 | $0 | $255,940 |

| Other Current Assets | $0 | $0 | $309,137 |

| Total Current Assets | $0 | $0 | $967,717 |

| Long-term Assets | |||

| Long-term Assets | $0 | $0 | $465,575 |

| Accumulated Depreciation | $0 | $0 | $181,651 |

| Total Long-term Assets | $0 | $0 | $283,924 |

| Total Assets | $0 | $0 | $1,251,641 |

| Current Liabilities | |||

| Accounts Payable | $0 | $0 | $336,000 |

| Current Borrowing | $0 | $0 | $0 |

| Other Current Liabilities (interest free) | $0 | $0 | $100,362 |

| Total Current Liabilities | $0 | $0 | $436,362 |

| Long-term Liabilities | $0 | $0 | $452,036 |

| Total Liabilities | $0 | $0 | $888,398 |

| Paid-in Capital | $0 | $0 | $100 |

| Retained Earnings | $0 | $0 | $88,096 |

| Earnings | $0 | $0 | $275,047 |

| Total Capital | $0 | $0 | $363,243 |

| Total Capital and Liabilities | $0 | $0 | $1,251,641 |

| Other Inputs | |||

| Payment Days | 0 | 0 | 60 |

| Sales on Credit | $0 | $0 | $0 |

| Receivables Turnover | 0.00 | 0.00 | 0.00 |

2.3 Company Locations and Facilities

Our Insurance and Real Estate brokerage operates from two central locations. Our modern attractive office in Smalltown, at 178 Small Street, is located in a small plaza which is owned by the principals of our brokerage. It comprises 2,000 square feet.

In Nexttown, we operate from an 800 square foot, one-story brick veneer building overlooking Lake Small, which again is owned by the principals of our firm. The office is strategically located across from the Post Office.

Our Smalltown operation enjoys its own private parking lot for our clients and our staff. A second story was recently added to our office which will allow ample room for expansion. It is presently used for training, staff meetings, and conferences.

Services

Acme Insurance is committed to providing professional sales and service for its insurance customers. We have established what we consider to be an excellent reputation in our area, and are the largest multi-line insurance broker in our trading area.

3.1 Service Description

Acme Insurance provides home, automobile, and business insurance in Smalltown District. We take pride in knowing that for over 50 years we have helped our clients to find the best coverage at the right price that suits their needs and expectations. In the event of a claim, our clients know that we are there to provide help and counsel to ensure a fast, speedy claim settlement.

Like other independent brokers, we issue binders and new policies, endorsements and process renewals.

We have stressed to our insureds the importance of good communication between the broker and client to insure proper coverage is in place. We have noticed as our clients become better informed about insurance that there has been a tremendous increase in clients wishing in-depth discussions about their policy coverage and how they can get the most value for their insurance dollar.

We also provide insurance services to non-clients, such as lawyers and mortgagees, to ensure our mutual clients have proper coverage and binding notes in place for the purchase of homes, businesses, and automobiles.

3.2 Competitive Comparison

Our company’s strength lies in the quality and depth of our products and staff. Our offices, unlike our competition, are open six days a week. Because of our larger staff, we are able to service our clients even when a client’s broker is busy or out of the office on inspections.

Our staff has specialists in commercial insurance that can properly service and underwrite local business. We also have some quality commercial markets unavailable to our competition.

Since we are brokers, (not agents such as Co-operators), we have access to a range of standard and specialty markets.

Our Real Estate division, which is a separate company, helps with market value and replacement cost analysis when required.

3.3 Sales Literature

We have recently produced a pamphlet titled “Insurance Partners” which stresses that a successful insurance partnership between the client, the broker, and the company is based upon a new concept.

Not only do the broker and the company take responsibility for proper protection and indemnity in the event of loss, but in the 1990’s, the client must also take his share of responsibility to insure the safety of his property by keeping it well maintained and using qualified professionals to update or change the heating, electrical, and plumbing systems in his home. We stress that multiple claims or claims arising out of poor maintenance may adversely affect his insurance.

In addition to the above, our brokerage uses a number of boilerplate letters on our computer system that are sent along with various types of policies explaining unique features or limitations in the contracts to avoid possible Errors and Omissions claims. They also encourage our clients to contact us about reviewing their coverage and promote other products and services we provide.

3.4 Fulfillment

The key to fulfilling our clients needs is provided by our principals who have over 60 years experience between them as general insurance brokers, and our staff, many of whom have been insurance brokers well over 10 years. We have one staff member with her A.I.I.C., three staff with their C.A.I.B., and two more taking C.A.I.B. courses. One staff member is completing courses to have the restriction removed from his license so he can be an alternate designated individual.

We call upon the ample resources of our insurance markets to help with any unusual situations which occur and may present a problem finding proper coverage for our client.

When we required trained inspectors for evaluating the safety of our insured’s solid fuel heating devices and installations, we sent one of our own producers for training and who now has W.E.T.T. certification.

We are proud that Acme Insurance Inc. has never had an errors and omissions loss, but to protect our clients against that possibility, we have in place Errors and Omissions Insurance through our Insurance Brokers Association in the amount of $1,000,000 (Employer’s Reinsurance).

3.5 Technology

We have been fully computerized since 1982 and both offices and some of our producer’s homes are connected to our main computer server located in Smalltown.

As of February 1996, we have entered into an agreement with our present computer vendor, Teleglobe, to update our computer system to a Pentium server, and to Release 74, which allows upload/download capability with our companies, as well as email.

We have elected to stay with the Teleglobe Tabs system since our staff is familiar with the program. It has exhibited excellent, reliable telecommunications ability. The high speed ISDN lines required for MS Windows-based communication between our branch office as well as our home offices are not available in our trading area, so at present we will not migrate to the new MS Windows-based products available from Teleglobe or Agency Manager.

3.6 Future Services

Although Stan Smith started out as a life insurance agent, the “life” part of our business represents only 1% of our sales. We are looking to strengthen this part of our operation in the future. Due to the complexity and number of life and disability products, we are presently using an outside service: Atlantic-Smith Insurance out of North Town, although two of our general insurance producers have life agent licenses.

We are in the process of setting up a substandard property market. We feel that there is a need for this service and that it can be profitable if strictly underwritten with proper controls in place.

Market Analysis Summary

Recent demographic studies in our area reveal a total year-round population of approximately 13,000, which rises in the summer to approximately 25,000. We have a relatively high number of seniors and many younger, newly-formed families dependent on government assistance living mostly in a rural, unserviced, thinly populated area. This makes it costly to service our clients. Long distance phone bills represent our second largest expense (our two offices each have their own toll free phone numbers) and the cost of visiting our insureds to do home inspections is time consuming due to the large area we service.

We are targeting seniors which have proven to be a profitable, stable market for our brokerage in spite of our present difficult economy.

We are fortunate that we have not yet had the intrusion to a large degree of mass merchandising programs like “Silver Power.” Smaller brokers have made inroads into our traditional rural business, with low cost farm markets that sell home and auto insurance. We understand that some of these markets are in a poor financial position and may cease to be a factor in the future.

4.1 Market Segmentation

Our market consists of senior citizens, lower-income young families (many of who are on social assistance) and the small, family-run business (many of which are seasonal and based on the tourist trade). There are a few industrial risks and those that are located here are branches of larger industries which obtain their insurance through large brokers in Bigtown.

Our target market is the seniors, family business, and middle income earners in our area. Statistics show that over 42% of our permanent population is above 45 years of age. The average family income is approximately $27,000 and the unemployment rate 9%.

We are cautious about encouraging business from lower income prospects since they tend to have wood heat, homes in poor repair, and many attempt to install and repair their own plumbing, wiring, and heating systems.

Another market of concern is out-of-area clients who may have been payment or claim problems to local brokers and attempt to find a distant broker to provide coverage instead of making the necessary adjustments in their own lifestyle to prevent claims.

Clients who have moved repeatedly can be difficult to obtain proper underwriting information and past claims experience on, and we feel our staff is to be commended for their ability to properly assess if a client should be placed to our standard markets or would be better served by a specialty company.

| Market Analysis | |||||||

| 1996 | 1997 | 1998 | 1999 | 2000 | |||

| Potential Customers | Growth | CAGR | |||||

| Ages 0 to 14 | 2% | 2,550 | 2,601 | 2,653 | 2,706 | 2,760 | 2.00% |

| Ages 15 to 44 | 2% | 4,760 | 4,855 | 4,952 | 5,051 | 5,152 | 2.00% |

| Ages 45 to 64 | 5% | 2,885 | 3,029 | 3,180 | 3,339 | 3,506 | 4.99% |

| Ages 65 to 74 | 5% | 1,280 | 1,344 | 1,411 | 1,482 | 1,556 | 5.00% |

| Other | 2% | 1,000 | 1,020 | 1,040 | 1,061 | 1,082 | 1.99% |

| Total | 3.03% | 12,475 | 12,849 | 13,236 | 13,639 | 14,056 | 3.03% |

4.2 Service Business Analysis

The past few years have seen tremendous upheaval in the insurance industry. The number of players has decreased in both the broker and company communities. The automobile product has, in the mind of the public, become unaffordable, unavailable, and impossible to understand. The recession has curtailed insureds from properly maintaining their homes and automobiles, and to exacerbate the situation, many clients have turned to wood heat and started doing their own repairs and maintenance which may have increased the number and severity of claims. Insurance fraud has become a major issue for the entire insurance industry.

Our traditional close relationship with our companies has been strained. Brokers are concerned that in spite of commission reductions, quotas, contract cancellations, and refusal to write new auto business by some markets, they now may find themselves in competition with some of the traditional broker distribution companies that are setting up direct marketing facilities and branches. The banks, even though thwarted by the federal government in its last budget to retail insurance from their premises, will continue pressure on the government and now have announced they will open stand alone insurance offices to retail insurance.

In spite of the above, we believe that the independent broker will survive. We are more automated than most service industries. We are close to the customer, regardless of some insurance companies’ attempts to sever the traditional broker-client relationship. Our clients, in most cases, still do not care or know which company we place them with. They trust our judgement in selecting the proper coverage and company to place them in.

The new federal government is close to adopting a new automobile contract that hopefully will make it affordable, understandable, and available to our clients. A profitable automobile product will entice the companies to aggressively seek new sales and more brokers will see companies offering contracts.

Upload/download capabilities are in many brokers offices, including our own. This will cut costs, improve efficiency and accuracy, and help us meet the competition from banks and direct writers. Companies that truly value and trust the broker distribution system will align themselves with professional brokers and grant more underwriting authority similar to Lloyds.

4.2.1 Main Competitors

Local independent brokers

Cal Roberts, Patrick C. Johnson, Rob Champlain

- Strengths – alternate markets, especially small farm mutuals, that still continue to give low prices, still continue to write wood stoves, and allow discounts and underwriting terms such as table 1 rates on homeowners within 8 km of fire hall protection.

- Weakness – most are smaller, one-man operations that do not have the backup or finances to aggressively impact the marketplace.

Agents (such as Co-operators)

- Strengths – Large advertising budget and competitively priced products. Their commercial is difficult to compete against in some cases because they seem to not have the same restrictions on underwriting as our markets. Also they have large capacity to write certain risks.

- Weakness- one small operation that does not have the same hours as our offices. Staff, because of salary, do not appear to be very knowledgeable or aggressive.

Mass Markets

- Strengths – large advertising budget and very competitive prices.

- Weakness – not local and largely unknown to our clients at the present time.

Our own Companies

- Strengths – already known to our clients; will be competitively priced.

- Weakness – an unknown quantity to our insureds. Also, if their people skills are similar to what they now exhibit, they will have great difficulty empathizing with the client and selling the client what he needs, not what they think he needs.

Mass merchandise programs heavily advertised over the radio such as “Gray Power”

- Strengths – price.

- Weakness – a still untried, unknown quantity.

Group Plans – teachers, public employees

- Strength – group pricing.

- Weakness – very little obviously, since we insure very few of the professions.

4.2.2 Competition and Buying Patterns

The main volume of income for our brokerage is generated by automobile premiums because they are relatively higher priced to insure than property, and because automobile insurance is mandatory in the region.

As stated previously, our success is dependent on our staff and our companies convincing our clients and prospective clients that price, although important, is not the only criteria for the purchase of insurance. Our advertising stresses that we have two offices, open six days a week with after-hours support and we have been an active, concerned, community involved, local business since 1938.

Still, price is very important and we must work with our markets to ensure that our insurance products are available and affordable to a large part of the market. It is the broker’s job to ensure the client understands what he is buying, and if circumstances dictate a lower-priced product, we must make our insured aware of the trade-off in coverage versus price.

4.2.3 Business Participants

- Cal Roberts Insurance

- Markets – Royal, Dominion of Canada

- Patrick C. Johnson

- Markets – General Accident, Canadian Surety

- Rob Champlain

- Markets – Farmer’s Mutual, National Frontier

- Co-Operators

- Silver Power

- Markets – Trafalger

- Con-struct Direct

4.2.4 Distributing a Service

Our trading area is rural. Premiums are relatively low and therefore not subject to large brokerages or specialty direct writers mounting aggressive advertising campaigns to bring in business. There are few group plans providing insurance coverage with the exception of our teachers. Smalltown has two independent brokers and a Co-Operators agent, Nexttown has two independent brokers, and Southtown has one. We have just started to see some move by locals to “Silver Power” and other specialty retailers who advertise on radio and television. The banks are still a future unknown.

Strategy and Implementation Summary

- Emphasize service and ongoing support. We must avoid selling only one policy at the lowest price for each customer and concentration account selling which greatly enhances client retention.

- Build an Insurance Partnership. The customer does not want to shop every year for a new broker. Concentrate on building a long term relationship with our customers and make the client and our staff appreciate the value of a long-term relationship.

- Focus on target markets. We must focus on personal and business customers that we identify and select to insure, instead of allowing potential customers to choose us, which could result in our brokerage attracting problem clients from other brokers.

5.2 Marketing Strategy

- Emphasize service and support.

- Build a partnership business based on account selling.

- Focus on senior, claims-free personal lines business and the profitable, well-run, small family business.

- Target small, non-franchise business that does not have access to group insurance plans.

- Investigate acquiring other brokerages in our area.

5.2.1 Promotion Strategy

We have depended in the past on a small advertisement in our local newspaper, listings in the Yellow Pages, and word of mouth. We must begin to investigate alternate ways to put our name in front of the public.

- All advertising has to emphasize our differentiation point rather than price. We will be developing a “Now what do I do?” message to emphasize the need for dealing with Acme’s insurance professionals so that in the event a loss occurs, you know you have the proper protection.

- We must sell the company, not the product. In spite of some companies’ efforts to minimize the importance of the broker, our clients still identify with the broker, not the insurance company.

- We must improve and increase our contacts with our clients. All clients should be contacted before renewal to ensure covers are current and adequate. Also, new insurance should be solicited. We are investigating the production of a company newsletter or use of the I.B.A.O. newsletter which is distributed on a bi-annual basis.

- We have put our email address in our newspaper advertising, but we must be careful about attracting clients from out of the area who may be difficult to service and properly inspect.

- Make contacts and support senior citizen groups and cottage associations. Identify sports and hobby groups that involve seniors and cottagers.

5.2.2 Distribution Strategy

- Select Seniors We will give special attention to this market in our advertising. We will make a concerted effort to support and sponsor seniors programs in our area. We will seek out Cottage associations and offer support and advice to attract new senior clients who are recently retired or about to in the near future.

- Insurance Partners We will include inserts in renewal, endorsements, and correspondence stressing the importance of the insured taking an active interest and responsibility for trying to control the severity and number of claims. Our staff should take every opportunity, when discussing insurance with a client, to emphasize the consequences of multiple claims.

- Business Partners Again we should encourage insureds to take responsibility for controlling claims in partnership with their broker by installing alarm systems and continuing to maintain and upgrade their property. We should stress the benefit that good loss ratios help to control rates and ensure markets that want to write their business.

5.2.3 Positioning Statement

Our target market is Smalltown District. The ideal client is claims-free aged between 45 – 75 who owns his own home and car and is debt free. Has exhibited stable family patterns and is known and respected in the community.

A similar profile should be used for commercial prospects with emphasis placed on the well-run, profitable business that has exhibited good claims experience.

5.2.4 Pricing Strategy

Our customers are especially sensitive to value. We must ensure that our price and service are perceived to be good value to our client.

Our markets must offer several payment options to our clients that are convenient to the client, not just to the company. Example – payment on insured’s preferred day of month, not on the company’s, and accepting payment by credit or debit card. Many insureds are on a fixed income and receive their income on a set day of each month or a paycheck on a particular day.

We encourage our companies to “Target Market.” Many of our companies are now focusing on what they have perceived to be profitable niche markets, where they can offer a competitive product with little, if any, competition.

We are seeing our commercial markets now moving toward basic coverage and limiting the “bells and whistles,” all-risk products available to only those clients who have modern, well-managed, profitable, low-risk operations. This should help stabilize pricing and, even more important, ensure that there is an insurance market available for most risks. Continued insistence by the industry on better protection, i.e. fire and burglar alarms, upgrading of buildings, etc., have started to lower loss ratios.

Many of the larger insurance markets have increased minimum premiums to $1,000 for any commercial package policy. Our Lloyds market should be able to accommodate these customers with a minimum premium of approximately $600.

5.3 Sales Strategy

We want to emphasize the benefit of dealing with professionals who live and work in our client’s area. We know their needs and their problems and we have a local reputation to protect, unlike an out-of-town market. If the out-of-town broker fails to provide proper cover or advice, they lose one client. We could stand to lose many if the public perceives a professional failure on our part.

Competitive prices for our identified target markets. Discounts of up to 25% for claims-free seniors who renew their home insurance with us.

Careful inspection and the judicious use of deductibles and warranties for insureds using wood stoves should help alleviate company concerns about solid fuel heating devices. Competitive pricing is not an important factor to attract business because competition is very limited for primary wood heat houses in our area. This may provide a chance to pick up all of the insured’s business because, in many instances, they contact us after being told by their previous broker that, in spite of their claims-free status, the broker doesn’t want their house insurance.

Business partners provide us the opportunity to sell lower-priced, basic insurance coverage to our client. Many clients have expressed interest in retaining part or all of the insurance risk, especially for burglary. They feel that if they have installed central alarms and bars, they can take the chance of self insurance.

5.3.1 Sales Programs

We are investigating sales incentives for our producers. They must encourage profitable new business and have a retention component. Presently, our producers receive $10 for every new policy written in our office, with the exception of recreational vehicles.

5.3.2 Sales Forecast

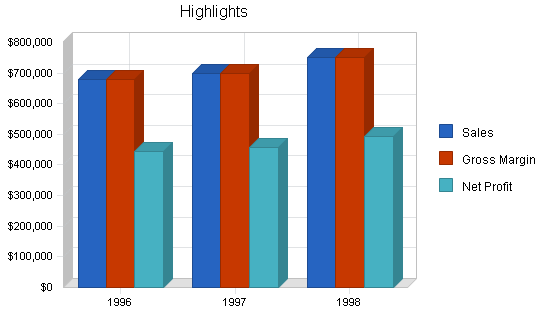

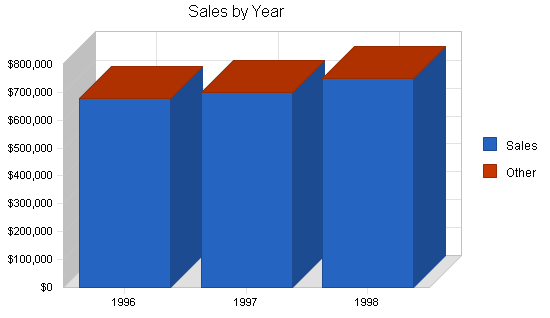

The following table and related charts show our present sales forecast. We are projecting sales to grow at a moderate but steady pace for the coming year and to continue into 1997.

| Sales Forecast | |||

| 1996 | 1997 | 1998 | |

| Sales | |||

| Sales | $677,600 | $700,000 | $750,000 |

| Other | $0 | $0 | $0 |

| Total Sales | $677,600 | $700,000 | $750,000 |

| Direct Cost of Sales | 1996 | 1997 | 1998 |

| Sales | $0 | $0 | $0 |

| Other | $0 | $0 | $0 |

| Subtotal Direct Cost of Sales | $0 | $0 | $0 |

5.4 Strategic Alliances

Some of our present companies have surveyed us to investigate co-operative advertising but we have not committed to any programs at present.

5.5 Service and Support

Acme Insurance is really a group of small brokerages housed under one name and location. Our producers are each responsible for a book of business. They sell, service, handle claims and are responsible for their accounts receivable. We have found over the years that our clients prefer to deal with one broker who is aware of their particular needs.

5.6 Milestones

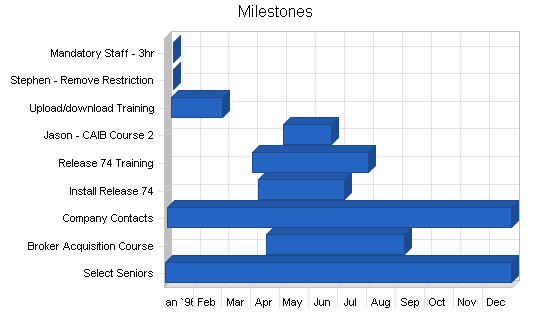

We have listed our plan milestones in the table below.

| Milestones | |||||

| Milestone | Start Date | End Date | Budget | Manager | Department |

| Select Seniors | 1/1/1996 | 12/31/1996 | $0 | P. Smith | Sales |

| Broker Acquisition Course | 4/17/1996 | 9/9/1996 | $250 | P. Smith | Finance |

| Company Contacts | 1/3/1996 | 12/31/1996 | $1,000 | P. Smith | Marketing |

| Install Release 74 | 4/8/1996 | 7/8/1996 | $0 | J. Smith | Staff |

| Release 74 Training | 4/2/1996 | 8/2/1996 | $300 | Staff | Staff |

| Jason – CAIB Course 2 | 5/4/1996 | 6/24/1996 | $395 | J. Smith | Staff |

| Upload/download Training | 1/7/1996 | 3/1/1996 | $1,000 | J. Smith | Staff |

| Stephen – Remove Restriction | 1/9/1996 | 1/10/1996 | $400 | Staff | Staff |

| Mandatory Staff – 3hr | 1/10/1996 | 1/10/1996 | $1,000 | P. Smith | Management |

| Totals | $4,345 | ||||

5.7 Service and Support

Acme Insurance is really a group of small brokerages housed under one name and location. Our producers are each responsible for a book of business. They sell, service, handle claims and are responsible for their accounts receivable. We have found over the years that our clients prefer to deal with one broker who is aware of their particular needs.

Management Summary

Acme Insurance is slow to hire new people and loyal to those whom we have hired. We hire only when there is a vacancy or growth dictates more staff. Most of our people have been in our organization over 15 years, which allows our clients and our companies to form long lasting business relationships with their broker.

6.1 Organizational Structure

Our brokerage is divided by client instead of service. Each broker is responsible not only to renew and service a client’s insurance, they also are responsible for collection and claims. We feel a client wants to deal with his or her broker, especially in a claim situation, instead of an unknown “specialist” whom they feel does not represent their interests.

Appendix

| Sales Forecast | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Sales | |||||||||||||

| Sales | 0% | $54,000 | $28,500 | $44,500 | $45,000 | $57,000 | $65,000 | $67,000 | $65,000 | $70,000 | $80,000 | $55,000 | $46,600 |

| Other | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Sales | $54,000 | $28,500 | $44,500 | $45,000 | $57,000 | $65,000 | $67,000 | $65,000 | $70,000 | $80,000 | $55,000 | $46,600 | |

| Direct Cost of Sales | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |

| Sales | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal Direct Cost of Sales | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Personnel Plan | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Name or Title or Group | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Name or Title or Group | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Name or Title or Group | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Total People | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Total Payroll | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Pro Forma Profit and Loss | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Sales | $54,000 | $28,500 | $44,500 | $45,000 | $57,000 | $65,000 | $67,000 | $65,000 | $70,000 | $80,000 | $55,000 | $46,600 | |

| Direct Cost of Sales | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other Costs of Sales | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total Cost of Sales | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Gross Margin | $54,000 | $28,500 | $44,500 | $45,000 | $57,000 | $65,000 | $67,000 | $65,000 | $70,000 | $80,000 | $55,000 | $46,600 | |

| Gross Margin % | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | |

| Expenses | |||||||||||||

| Payroll | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Marketing/Promotion | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Depreciation | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Rent | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Utilities | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Insurance | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Payroll Taxes | 15% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Other | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total Operating Expenses | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Profit Before Interest and Taxes | $54,000 | $28,500 | $44,500 | $45,000 | $57,000 | $65,000 | $67,000 | $65,000 | $70,000 | $80,000 | $55,000 | $46,600 | |

| EBITDA | $54,000 | $28,500 | $44,500 | $45,000 | $57,000 | $65,000 | $67,000 | $65,000 | $70,000 | $80,000 | $55,000 | $46,600 | |

| Interest Expense | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | $3,767 | |

| Taxes Incurred | $15,070 | $7,420 | $12,220 | $12,370 | $15,970 | $18,370 | $18,970 | $18,370 | $19,870 | $22,870 | $15,370 | $12,850 | |

| Net Profit | $35,163 | $17,313 | $28,513 | $28,863 | $37,263 | $42,863 | $44,263 | $42,863 | $46,363 | $53,363 | $35,863 | $29,983 | |

| Net Profit/Sales | 65.12% | 60.75% | 64.07% | 64.14% | 65.37% | 65.94% | 66.06% | 65.94% | 66.23% | 66.70% | 65.21% | 64.34% | |

| Pro Forma Cash Flow | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Cash Received | |||||||||||||

| Cash from Operations | |||||||||||||

| Cash Sales | $13,500 | $7,125 | $11,125 | $11,250 | $14,250 | $16,250 | $16,750 | $16,250 | $17,500 | $20,000 | $13,750 | $11,650 | |

| Cash from Receivables | $127,970 | $129,320 | $39,863 | $21,775 | $33,388 | $34,050 | $42,950 | $48,800 | $50,200 | $48,875 | $52,750 | $59,375 | |

| Subtotal Cash from Operations | $141,470 | $136,445 | $50,988 | $33,025 | $47,638 | $50,300 | $59,700 | $65,050 | $67,700 | $68,875 | $66,500 | $71,025 | |

| Additional Cash Received | |||||||||||||

| Sales Tax, VAT, HST/GST Received | 0.00% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| New Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Other Liabilities (interest-free) | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Long-term Liabilities | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Sales of Other Current Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Sales of Long-term Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Investment Received | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal Cash Received | $141,470 | $136,445 | $50,988 | $33,025 | $47,638 | $50,300 | $59,700 | $65,050 | $67,700 | $68,875 | $66,500 | $71,025 | |

| Expenditures | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |

| Expenditures from Operations | |||||||||||||

| Cash Spending | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Bill Payments | $336,628 | $18,582 | $11,347 | $15,992 | $16,257 | $19,817 | $22,157 | $22,717 | $22,187 | $23,737 | $26,387 | $19,053 | |

| Subtotal Spent on Operations | $336,628 | $18,582 | $11,347 | $15,992 | $16,257 | $19,817 | $22,157 | $22,717 | $22,187 | $23,737 | $26,387 | $19,053 | |

| Additional Cash Spent | |||||||||||||

| Sales Tax, VAT, HST/GST Paid Out | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Principal Repayment of Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Long-term Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Purchase Other Current Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Purchase Long-term Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Dividends | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal Cash Spent | $336,628 | $18,582 | $11,347 | $15,992 | $16,257 | $19,817 | $22,157 | $22,717 | $22,187 | $23,737 | $26,387 | $19,053 | |

| Net Cash Flow | ($195,158) | $117,863 | $39,641 | $17,033 | $31,381 | $30,483 | $37,543 | $42,333 | $45,513 | $45,138 | $40,113 | $51,972 | |

| Cash Balance | $207,482 | $325,345 | $364,986 | $382,019 | $413,400 | $443,883 | $481,426 | $523,759 | $569,272 | $614,410 | $654,523 | $706,495 | |

| Pro Forma Balance Sheet | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Assets | Starting Balances | ||||||||||||

| Current Assets | |||||||||||||

| Cash | $402,640 | $207,482 | $325,345 | $364,986 | $382,019 | $413,400 | $443,883 | $481,426 | $523,759 | $569,272 | $614,410 | $654,523 | $706,495 |

| Accounts Receivable | $255,940 | $168,470 | $60,525 | $54,038 | $66,013 | $75,375 | $90,075 | $97,375 | $97,325 | $99,625 | $110,750 | $99,250 | $74,825 |

| Other Current Assets | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 | $309,137 |

| Total Current Assets | $967,717 | $685,089 | $695,007 | $728,160 | $757,168 | $797,912 | $843,095 | $887,938 | $930,221 | $978,034 | $1,034,297 | $1,062,910 | $1,090,457 |

| Long-term Assets | |||||||||||||

| Long-term Assets | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 | $465,575 |

| Accumulated Depreciation | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 | $181,651 |

| Total Long-term Assets | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 | $283,924 |

| Total Assets | $1,251,641 | $969,013 | $978,931 | $1,012,084 | $1,041,092 | $1,081,836 | $1,127,019 | $1,171,862 | $1,214,145 | $1,261,958 | $1,318,221 | $1,346,834 | $1,374,381 |

| Liabilities and Capital | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |

| Current Liabilities | |||||||||||||

| Accounts Payable | $336,000 | $18,209 | $10,814 | $15,454 | $15,599 | $19,079 | $21,399 | $21,979 | $21,399 | $22,849 | $25,749 | $18,499 | $16,063 |

| Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Other Current Liabilities | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 | $100,362 |

| Subtotal Current Liabilities | $436,362 | $118,571 | $111,176 | $115,816 | $115,961 | $119,441 | $121,761 | $122,341 | $121,761 | $123,211 | $126,111 | $118,861 | $116,425 |

| Long-term Liabilities | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 | $452,036 |

| Total Liabilities | $888,398 | $570,607 | $563,212 | $567,852 | $567,997 | $571,477 | $573,797 | $574,377 | $573,797 | $575,247 | $578,147 | $570,897 | $568,461 |

| Paid-in Capital | $100 | $100 | $100 | $100 | $100 | $100 | $100 | $100 | $100 | $100 | $100 | $100 | $100 |

| Retained Earnings | $88,096 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 | $363,143 |

| Earnings | $275,047 | $35,163 | $52,476 | $80,989 | $109,852 | $147,116 | $189,979 | $234,242 | $277,105 | $323,468 | $376,831 | $412,694 | $442,677 |

| Total Capital | $363,243 | $398,406 | $415,719 | $444,232 | $473,095 | $510,359 | $553,222 | $597,485 | $640,348 | $686,711 | $740,074 | $775,937 | $805,920 |

| Total Liabilities and Capital | $1,251,641 | $969,013 | $978,931 | $1,012,084 | $1,041,092 | $1,081,836 | $1,127,019 | $1,171,862 | $1,214,145 | $1,261,958 | $1,318,221 | $1,346,834 | $1,374,381 |

| Net Worth | $363,243 | $398,406 | $415,719 | $444,232 | $473,095 | $510,359 | $553,222 | $597,485 | $640,348 | $686,711 | $740,074 | $775,937 | $805,920 |